Ready in minutes

AI builds your ad from a single prompt

November 27, 2025

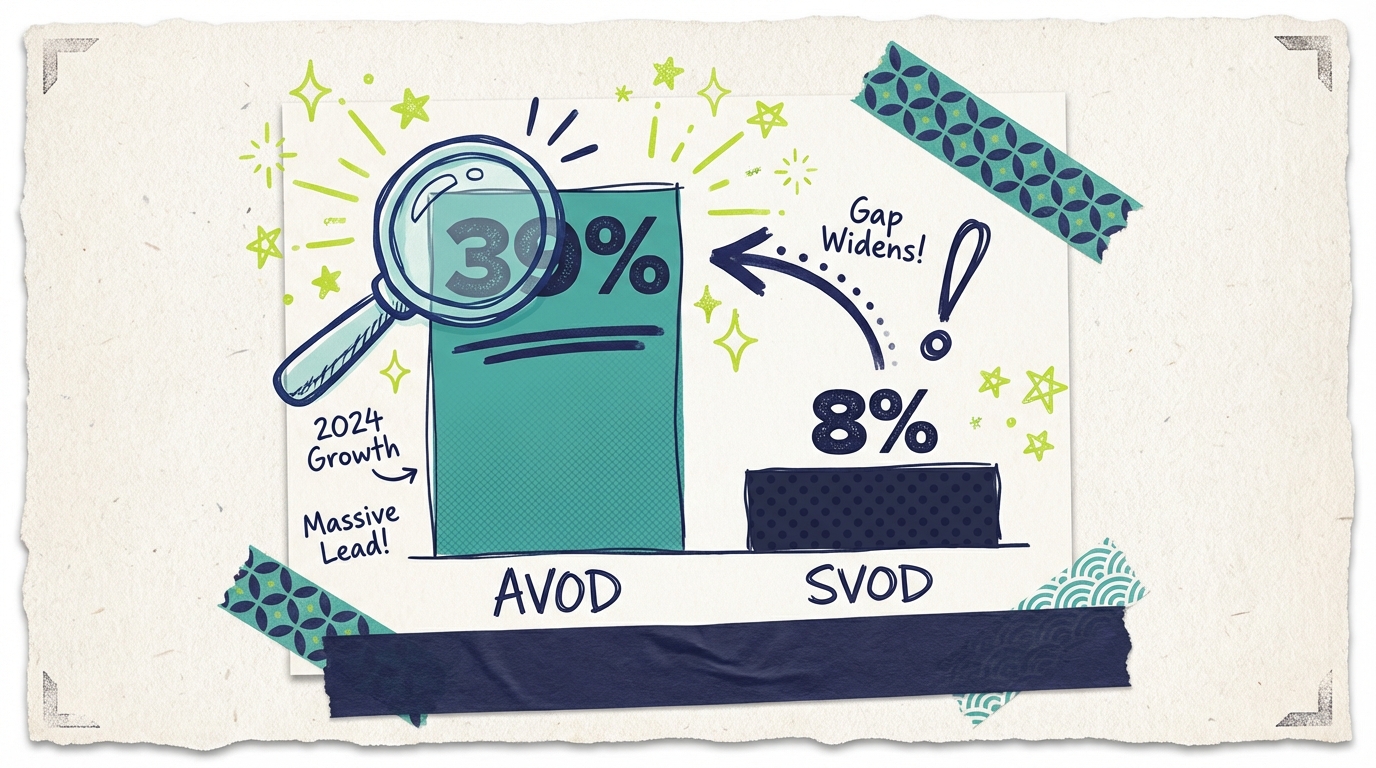

39%

AVOD revenue growth in 2024

$14.3B

Premium AVOD platform revenue

4x

AVOD growth vs SVOD growth rate

AVOD (advertising video-on-demand) revenue is growing significantly faster than traditional SVOD (subscription video-on-demand) revenue. In 2024, premium AVOD platform revenue grew 39% to reach $14.3 billion, according to MoffettNathanson research. Meanwhile, pure subscription revenue growth has plateaued as streaming services shift their focus to ad-supported tiers. The numbers tell a clear story: 71% of all net new streaming subscribers over the past nine quarters have come from ad-supported plans, according to Antenna research. For advertisers, this shift represents an unprecedented opportunity to reach premium streaming audiences at accessible price points.

The streaming industry is undergoing a fundamental transformation in how it generates revenue. After a decade of the subscription-first model, advertising has emerged as the primary growth engine for the entire industry.

Consider the numbers: premium AVOD platforms generated $14.3 billion in revenue in 2024, representing a 39% increase from the previous year according to MoffettNathanson analysis. That growth rate dwarfs what subscription tiers are achieving. For 2025, the same research projects AVOD spending will rise another 17% to exceed $15 billion across the top 11 streaming platforms.

The individual platform data reinforces this trajectory. Hulu leads all platforms with $3.1 billion in ad revenue for 2024. Peacock follows at $2.1 billion (up 114% year-over-year in Q3 alone), while Prime Video reached $2.0 billion despite only launching ads in January 2024. Netflix, which resisted advertising for years, generated $1.6 billion in its first full year of ad-supported streaming, with revenue growing 116% over 2023.

What makes this growth particularly significant is where it comes from. According to Antenna data, 65% of ad-supported subscribers are entirely new to the platforms they join. Another 23% are returning users who previously canceled, and just 11% downgraded from ad-free plans. This means advertising tiers are expanding the total addressable market rather than cannibalizing existing subscribers.

The global picture tells a similar story. The worldwide AVOD market was valued at $38 billion in 2023 and is projected to reach $69 billion by 2027, according to Statista. That represents compound annual growth exceeding 16%, a rate that subscription services simply cannot match as market saturation approaches in major economies.

Industry analysts project this divergence will continue widening. According to Streaming Media Global, global AVOD revenue will grow at a 14.1% compound annual growth rate through 2029, while subscription revenue growth levels off. By 2029, premium AVOD is projected to reach $141 billion compared to SVOD at $185 billion, meaning the gap is narrowing rapidly.

For context, this shift has happened remarkably quickly. As recently as 2019, ad-supported streaming was an afterthought. Netflix famously insisted it would never run ads. Disney+ launched ad-free only. The entire AVOD market was dominated by free services like Tubi and Pluto TV that were seen as second-tier destinations. The reversal took less than five years.

Understanding the full picture requires examining where AVOD growth is concentrated and how different platforms are contributing to the shift.

The top performers in ad revenue growth reveal which platforms are capturing the advertising opportunity most effectively:

Hulu: $3.1 billion in 2024 ad revenue (up 5% in Q3)

Peacock: $2.1 billion (Q3 ad revenue up 114% YoY)

Prime Video: $2.0 billion (up 133% YoY)

Netflix: $1.6 billion (up 116% YoY)

Roku Channel: $1.2 billion (up 22% in Q3)

Pluto TV: $1.0 billion (up 18% in Q3)

Tubi: Growing 24% with significant political advertising boost

What stands out is that every major platform is posting double-digit or higher growth in ad revenue. The platforms that launched ads most recently (Prime Video, Netflix, Disney+) show the fastest percentage growth, while established ad players like Hulu maintain their dollar-volume leadership.

The composition of streaming subscribers has shifted dramatically toward ad-supported plans. According to Antenna research via eMarketer:

46% of US streaming subscribers now pay for ad-supported tiers (up from negligible share five years ago)

57% of Q1 2025 gross subscriber additions chose ad-supported plans

71% of net new subscribers over the past nine quarters selected ad-supported options

86% of subscribers offered an ad-supported option accept it

75% of all streaming users have tried an ad-supported plan in the past four years

These numbers demolish the assumption that consumers universally prefer ad-free experiences. When given a price-sensitive option, most choose ads.

The scale of ad-supported streaming has reached levels that rival traditional television:

Amazon Prime Video: 130 million ad-supported viewers in the US alone

Disney (combined): 164 million monthly active users across Disney+, Hulu, and ESPN+

Netflix: 94 million global monthly active users on ad tier (up from 70 million six months prior)

Peacock: Expanding rapidly following Upfront commitments

Max (HBO): Growing ad tier as part of hybrid strategy

Combined, the major streaming platforms now reach hundreds of millions of ad-supported viewers monthly, creating inventory that approaches broadcast television scale with far superior targeting capabilities.

While AVOD surges, traditional subscription metrics show strain:

Average number of SVOD subscriptions per US household fell by more than 10% in 2024

Ad-free pricing increases (often 15-20%) are outpacing ad-supported tier increases (often 5-10%)

Customer acquisition costs for pure subscription models continue rising

Churn rates remain elevated as consumers rationalize their streaming stacks

The subscription model isn't dying, but its growth days are largely over in mature markets. Future revenue growth for streaming platforms will be advertising-led.

This structural shift in streaming economics creates real opportunities for businesses of all sizes. The rise of AVOD means more advertising inventory, more sophisticated targeting, and more accessible price points than ever before.

Consider what's changed. Five years ago, reaching streaming audiences required either massive budgets for linear TV or accepting the limitations of programmatic digital advertising. Streaming platforms were subscription-only fortresses that advertisers couldn't access. Today, those same premium audiences watch ads on Netflix, Disney+, Prime Video, and dozens of other platforms, and the inventory is available programmatically at CPMs that work for local businesses.

The numbers on viewer attention are particularly compelling. According to CTAM research, 81% of free streaming subscribers and 69% of SVOD subscribers say they're willing to accept commercials. That's not grudging tolerance; it's active acceptance of the value exchange. Viewers understand that advertising enables lower prices and more content.

For local and regional businesses, the expansion of AVOD creates targeting possibilities that didn't exist on traditional TV. You can now reach streaming viewers by geography, demographics, interests, and behaviors. A restaurant can target food enthusiasts within a 15-mile radius. A dentist can reach families with children in specific zip codes. An HVAC company can target homeowners during the seasons when systems need service.

The pricing has followed the inventory expansion. With more AVOD supply coming online, average CPMs on streaming platforms have become more accessible. Where premium streaming inventory once commanded $50+ CPMs, many placements now fall in the $15-35 range for small business advertisers using self-serve platforms.

Platforms like Adwave let you run TV advertising starting at just $50, with AI-generated creative that eliminates production costs. You can reach the same Netflix, Hulu, and Prime Video viewers that major brands target, but with budgets appropriate for local businesses. The democratization of TV advertising that industry observers predicted for years is actually happening.

The growth of AVOD isn't just interesting data; it's an actionable opportunity. Here's how businesses can capitalize on the shift.

Start by understanding where your customers are watching. The fragmentation of streaming means different demographics gravitate toward different platforms. Younger viewers over-index on YouTube and free services like Tubi. Families with children concentrate on Disney+ and Peacock. Sports fans are increasingly finding content on streaming. Knowing your audience helps you prioritize where to focus.

For most small businesses, the smartest approach is starting with a test campaign rather than trying to optimize everything from day one. Set aside $200-500 for a two-week test across multiple streaming platforms. Use AI-generated creative to keep production costs at zero. Focus on a single geographic area and one clear message. The goal isn't to win the Super Bowl; it's to learn what resonates with your specific audience.

Target strategically based on what the data reveals. Evening hours from 7-10 PM capture the most engaged streaming viewers. Weekday viewing tends to skew older; weekend viewing attracts more families. Some content categories will align better with your target customers than others. Your initial campaign data will reveal these patterns.

Measure differently than you would for performance marketing. Streaming TV advertising builds brand awareness rather than driving immediate clicks. Watch for brand search lift (are more people Googling your business name?), increases in website traffic during and after your campaign, and simple customer surveys asking how new customers heard about you. The impact often shows up in your other marketing channels becoming more effective.

Scale deliberately when you find something that works. Increase budget on winning creative rather than spreading thin across variations. Expand geographic targeting once you've proven the message. Test additional platforms beyond your initial mix. The advertisers who succeed with streaming TV are patient enough to learn before they scale.

The AVOD surge represents more than a temporary market shift; it's a structural realignment of how video entertainment is monetized.

The subscription-only model that defined streaming's first decade is effectively over. Every major platform now offers an ad-supported tier, and several have made it the default. Netflix, which built its brand on the promise of no commercials, now generates over $1.6 billion annually from advertising. Disney has restructured its entire streaming strategy around ad-supported growth. Amazon made ads the default for 130+ million Prime Video viewers.

This isn't a temporary experiment. Platforms are restructuring their businesses around advertising revenue. They're hiring ad sales teams, investing in ad tech, and making advertising integral to their profitability. The streaming industry is converging toward a hybrid model where both subscriptions and advertising contribute meaningfully to revenue.

Several forces are pushing streaming toward advertising. First, subscription growth has plateaued in developed markets. The easy subscriber additions are gone. Second, content costs have exploded, making it harder to profit on subscriptions alone. Third, advertisers are desperate for premium video inventory as linear TV audiences decline. Fourth, consumers have shown clear preference for lower-priced ad-supported options when given the choice.

The economics now favor advertising. A streaming platform can generate more lifetime value from an ad-supported subscriber than from a premium subscriber who churns after a few months. Ad revenue is recurring and scalable in ways subscription revenue no longer is.

For advertisers, this shift is unambiguously positive. More AVOD inventory means more options, more competition among sellers, and ultimately better pricing. The democratization of streaming TV advertising continues as inventory expands and platforms develop self-serve tools.

The targeting and measurement capabilities on streaming far exceed traditional linear TV. Advertisers can reach specific audiences, track outcomes, and optimize campaigns in ways that broadcast advertising never allowed. As the industry matures, these capabilities will only improve.

Beyond traditional AVOD, free ad-supported streaming TV (FAST) continues explosive growth. According to Wurl research, monthly active FAST households grew 12% year-over-year, while daily viewing hours per household climbed 16%. The number of FAST channels has increased 14% over 2024 and is up 76% from 2023.

Services like Tubi, Pluto TV, and Roku Channel are capturing significant viewing share. Nielsen data shows FAST channels combined now capture more viewing time than individual premium streamers like Peacock, Max, or Paramount+. For advertisers seeking reach at accessible CPMs, FAST represents an increasingly important part of the mix.

Industry analysts are unanimous in identifying advertising as streaming's primary growth vector going forward.

MoffettNathanson, the research firm that tracks streaming economics most closely, projects AVOD spending will rise 17% in 2025 to exceed $15 billion across premium platforms. Their Q3 2024 analysis showed premium streaming ad revenues up nearly 50% year-over-year, reaching $3.8 billion in a single quarter.

"Online video is now an advertising-led business," concluded Streaming Media's year-end review. "As subscription revenue growth levels off, global AVOD revenue will continue to grow at a compound annual growth rate of 14.1%."

According to eMarketer analysis, the shift to ad tiers has become the default trajectory for the streaming industry: "Platforms are no longer treating ad-supported tiers as a budget option but as a core growth driver. If current patterns hold, the majority of streaming growth going forward will be driven by these hybrid models."

Omdia research confirmed the trend, reporting that "in the period 2025-30, ad-tier subscription revenue will grow at a faster pace than premium ad-free subscription revenue." The firm characterized streaming platforms' shift to advertising as a gamble that is "already paying off."

The consensus is clear: AVOD growth will outpace SVOD growth for the foreseeable future, and the streaming industry's economics are being rebuilt around advertising.

AVOD (advertising video-on-demand) refers to streaming content that's free or discounted because it includes advertising. Think of Tubi, Pluto TV, or the ad-supported tiers of Netflix and Disney+. SVOD (subscription video-on-demand) refers to ad-free streaming that's paid for entirely through subscription fees, like Netflix's premium tier or the original Disney+ model. Many platforms now offer both options, letting viewers choose between paying more for ad-free or paying less (or nothing) with ads.

Three main factors drive AVOD's faster growth. First, subscription fatigue has set in as households already pay for multiple streaming services and resist adding more at premium prices. Second, platforms have invested heavily in their ad tiers, making them attractive options with fewer ads than traditional TV. Third, advertisers are pouring money into streaming as linear TV audiences decline, creating demand that pulls supply. The combination of consumer price sensitivity and advertiser demand makes AVOD the growth engine.

No. Premium ad-free tiers will remain available for viewers willing to pay more. But they'll increasingly become the minority option as platforms price them at premiums designed to encourage ad-supported adoption. Expect ad-free pricing to continue rising faster than ad-supported pricing, widening the gap between tiers and naturally steering more subscribers toward ads.

Not necessarily. Streaming platforms are competing on ad experience, typically running 4-6 minutes of ads per hour compared to 15-20 minutes on traditional TV. The goal is maintaining a better viewing experience than linear TV while generating advertising revenue. Some platforms are experimenting with non-intrusive formats like pause ads and shoppable ads that don't interrupt content at all.

Yes. The expansion of AVOD inventory and the development of self-serve platforms have made streaming TV accessible to businesses of all sizes. Platforms like Adwave allow campaigns starting at $50 with no production costs. You won't have Super Bowl reach, but you can achieve meaningful frequency with local audiences at budgets appropriate for small businesses.

Streaming TV CPMs typically range from $15-45 for programmatic buying, compared to $10-30 for broad local TV and $30-75+ for national broadcast. Premium streaming placements (Netflix, Disney+) command higher CPMs ($25-65) while FAST channels and programmatic inventory often fall in the $15-30 range. For small businesses, the improved targeting usually makes streaming's slightly higher CPMs worthwhile because less budget is wasted on irrelevant viewers.

Additional context on AVOD and SVOD growth trends:

2024 AVOD revenue: $14.3 billion across top 11 premium streaming platforms (MoffettNathanson, Q3 2024)

2025 AVOD projection: $15+ billion, up 17% year-over-year (MediaPost, October 2025)

Global AVOD market: $38 billion in 2023, projected $69 billion by 2027 (Statista)

Ad-supported subscriber share: 46% of US streaming subscribers on ad-supported plans (Antenna via eMarketer, Q1 2025)

New subscriber source: 71% of net new SVOD subscribers over past 9 quarters chose ad-supported plans (Antenna, 2025)

Netflix ad tier: 94 million global monthly active users (eMarketer, May 2025)

Disney ad reach: 164 million monthly active users across Disney+, Hulu, ESPN+ (eMarketer, May 2025)

Prime Video ads: 130 million US ad-supported viewers (eMarketer, 2025)

FAST growth: Monthly active FAST households up 12% YoY, viewing hours up 16% YoY (Wurl via CTAM, 2025)

2029 projection: AVOD $141 billion vs SVOD $185 billion globally (Streaming Media Global, 2025)

All sources linked above. Data current as of Q4 2025.

Ready to reach streaming viewers on Netflix, Hulu, Disney+, and 100+ other premium channels? The growth of ad-supported streaming means more inventory at better prices than ever before.

Adwave makes TV advertising accessible for small businesses with campaigns starting at just $50. No production budget required since AI generates your commercial. No agency needed.