Ready in minutes

AI builds your ad from a single prompt

December 12, 2025

36%

U.S. adults still subscribed to cable/satellite

55%

Americans who stream but have no cable

44.8%

Streaming share of total TV viewing

Cord cutting is not slowing down, despite a surprising one-quarter uptick in pay TV subscribers. According to MoffettNathanson research, pay TV operators added 303,000 net subscribers in Q3 2025, the first quarterly gain since 2017. However, this blip masks the underlying reality: traditional cable and satellite continue their structural decline, with year-over-year subscriber losses still running at 5.8%. The Q3 "gain" came almost entirely from virtual pay TV services like YouTube TV, while actual cable companies merely slowed their bleeding. For advertisers, the message is clear: cord cutting has not reversed, streaming continues gaining share, and reaching television audiences increasingly requires CTV advertising rather than traditional TV buys.

The cord cutting picture requires understanding both the headline and the underlying dynamics.

The surprising Q3 2025 data shows pay TV operators gained 303,000 net subscribers, according to MoffettNathanson's "Cord-Cutting Monitor Q3 2025" report. This marks the first time since 2017 that the industry added subscribers quarter-over-quarter. The research firm noted, "There are more linear video subscribers now than there were three months ago. That's the first time we've been able to say that since 2017."

However, context matters enormously. The gain came primarily from virtual multichannel video programming distributors (vMVPDs) like YouTube TV, not traditional cable. YouTube TV alone added an estimated 750,000 subscribers in Q3 2025. Traditional cable and satellite operators continued losing subscribers, just at a slower pace than previous quarters.

The year-over-year comparison tells the real story. According to Ars Technica's analysis, pay TV's subscriber count was down 5.8% in Q3 2025 compared to Q3 2024. The previous year's decline was 6.7%. So while the rate of decline is slowing, the industry is still shrinking by millions of subscribers annually.

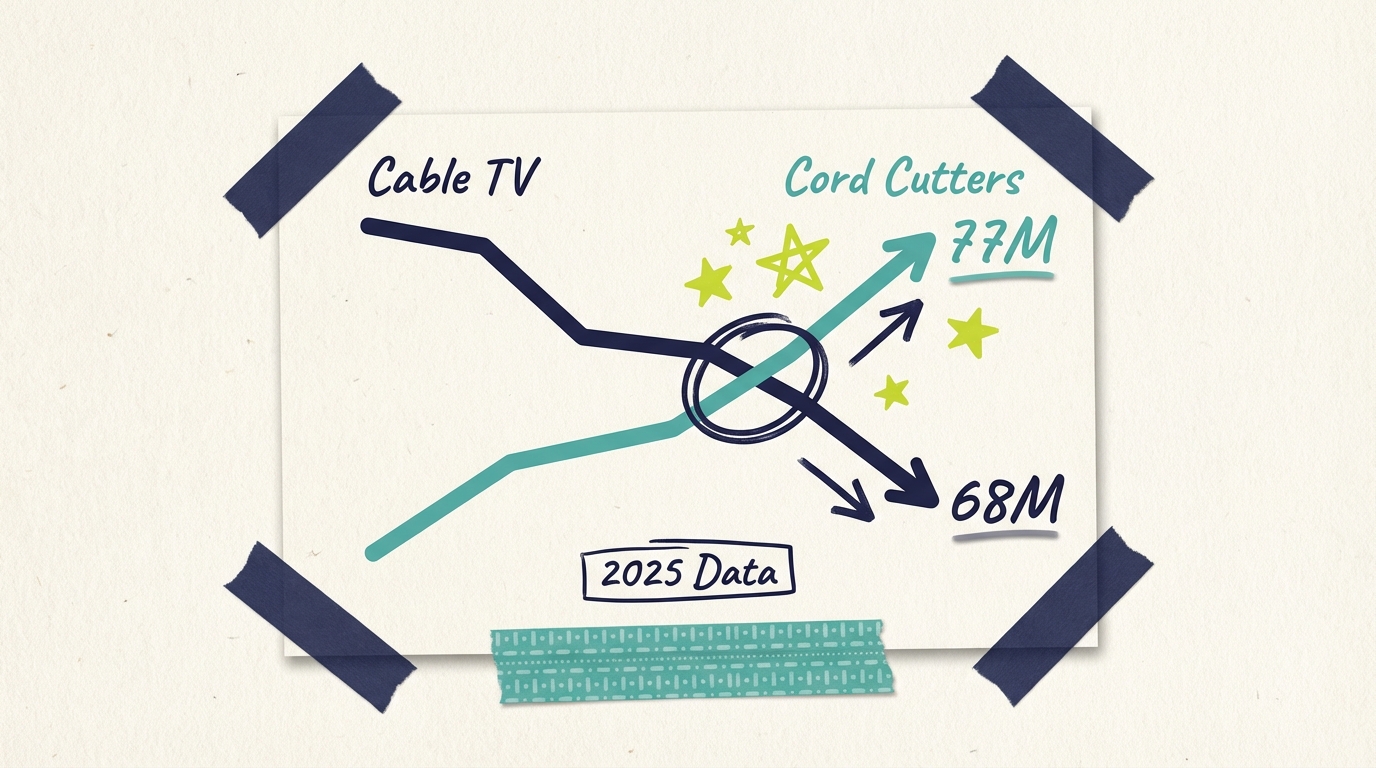

The absolute numbers illustrate the long-term trend. According to CableCompare, 68.7 million U.S. households still subscribe to cable TV in 2025. That sounds substantial until you compare it to the 105 million households subscribed in 2010. Pay TV has lost over a third of its customer base in 15 years.

Cable TV penetration rates have collapsed correspondingly. In 2010, approximately 88% of U.S. households subscribed to pay TV. By 2025, that figure has dropped to approximately 35%, according to nScreenMedia. The majority of American households now either cut the cord or never subscribed in the first place.

Cord-cutting households now outnumber cable households. An estimated 77.2 million U.S. households have cut the cord as of 2025, surpassing the 68.7 million that still subscribe to traditional pay TV. The crossover represents a fundamental shift in how Americans access television content.

Understanding the segments within cord cutting helps explain why the trend continues despite occasional slowdowns.

The pay TV landscape has fragmented significantly:

Traditional cable (Comcast, Charter, etc.): Continuing to lose subscribers, though Q3 2025 showed improvement. Charter reported net attrition of about 70,000 customers in Q3 2025, compared to 294,000 in Q3 2024. Comcast reported its best quarter in almost five years, losing "only" 257,000 subscribers. Better, but still declining.

Satellite (DirecTV, Dish): Facing steeper declines than cable. Dish in particular has struggled with subscriber losses and financial challenges. The satellite model faces structural disadvantages in a streaming world.

vMVPDs (YouTube TV, Hulu + Live TV, Fubo): The only segment actually growing. YouTube TV leads with an estimated 9.4 million subscribers, adding 750,000 in Q3 2025 alone. However, vMVPD growth has moderated from earlier years, and some services (like Fubo) have faced challenges maintaining pricing and content.

Cord cutting patterns vary dramatically by age:

Ages 18-34: The "cord-never" generation. Many have never subscribed to traditional pay TV and likely never will. Streaming is their default, and cable seems as antiquated as landline phones.

Ages 35-49: Active cord-cutters. This demographic remembers cable but has largely transitioned to streaming. Cost and flexibility drive their decisions.

Ages 50-64: Mixed behavior. Many have cut the cord, but significant numbers maintain cable subscriptions out of habit or for specific content like local news.

Ages 65+: Most likely to retain cable. This demographic has the highest cable retention rates, though even seniors are increasingly adopting streaming.

According to Adweek research, 50% of consumers under age 32 won't pay for cable TV. This cord-never phenomenon ensures that cable's subscriber losses will accelerate as older demographics age out of the market.

The motivations behind cord cutting have remained consistent:

Cost: 86.7% of cord cutters cite high cable costs as a significant reason for switching, according to Evoca research

Content availability: Streaming platforms offer more content that viewers actually want

Flexibility: No contracts, cancel anytime, watch anywhere

User experience: Better interfaces, recommendations, and on-demand access

Advertising load: Streaming offers ad-free options or lighter ad loads

The cost factor deserves emphasis. Average cable bills run $100-150+ monthly for bundles that include hundreds of channels viewers never watch. Streaming allows households to pay for exactly what they want, typically at significant savings.

The subscriber losses translate directly to revenue decline. According to Evoca research, pay TV revenue dropped from $100.09 billion in 2017 to $84.29 billion in 2024, a 16.5% decline in just eight years. By 2027, revenue is projected to fall further to $81.33 billion.

For cable operators, the mathematics are brutal. Fixed costs (infrastructure, content rights, personnel) don't decline proportionally with subscriber losses. Each lost subscriber increases the cost burden on remaining customers. Higher prices accelerate cord cutting. The negative spiral has no obvious end point.

This revenue pressure explains why cable companies are diversifying aggressively into broadband, mobile, and streaming partnerships. Comcast, Charter, and others recognize that cable TV as a standalone business faces structural decline that strategy adjustments cannot reverse.

Cord cutting trends directly impact how businesses can reach television audiences.

The fundamental shift is straightforward: if your target customers are cutting the cord, cable TV advertising can't reach them. And the data shows that most Americans under 50 have either cut the cord or never subscribed. A local TV advertising strategy focused exclusively on cable increasingly misses the majority of the market.

Consider the math for a business targeting adults 25-54, a common advertising demographic. Among this group, streaming now dominates viewing time. According to Nielsen, streaming captured 47.3% of all TV viewing in mid-2025, compared to cable's 26.7% and broadcast's 20.1%. A cable-only advertising strategy reaches less than half the potential audience.

The implications compound over time. Every year, more households cut the cord. Every year, more young adults enter the market as cord-nevers. Every year, cable's reach diminishes while streaming's expands. Businesses that establish streaming TV presence now will be positioned for where audiences are going, not where they were.

For local businesses specifically, streaming offers advantages beyond raw reach. Geographic targeting on CTV allows a restaurant to reach households within delivery radius specifically, not waste money on viewers across town. Time targeting enables reaching audiences during meal-decision hours. Frequency capping prevents oversaturation that drives negative response.

The cord cutting trend isn't temporary, despite Q3's surprising numbers. The structural drivers (cost, flexibility, content) aren't reversing. The demographic wave (cord-nevers entering adulthood) continues building. Smart businesses are transitioning their TV advertising budgets to streaming now, not waiting for cable to decline further.

Capitalizing on cord cutting requires shifting advertising strategy toward streaming audiences.

Audit your current TV spend. If you're buying cable TV advertising, honestly assess who you're reaching. Request audience data from your cable provider or media buyer. Compare cable's delivery against where your target customers actually spend viewing time. Many businesses discover they're paying for audience they can't reach.

Start streaming advertising alongside existing efforts. You don't need to abandon cable immediately. Begin testing CTV campaigns while maintaining current buys. Compare performance. Let data guide your transition pace.

Focus on cord-cutter households specifically. Some streaming platforms and DSPs allow targeting of households that don't subscribe to traditional TV. This cord-cutter targeting ensures your streaming investment reaches incremental audiences that cable can't deliver.

Leverage the cost advantage. Streaming TV advertising through platforms like Adwave starts at just $50, compared to typical cable minimums of $5,000-10,000. Use the lower barrier to entry for testing and learning before committing significant budget.

Develop creative for streaming environments. The non-skippable, lean-back streaming context differs from cable. Viewers will watch your entire ad, so make every second count. Focus on brand building and clear value propositions rather than urgency-driven calls to action.

Plan for continuing decline. Budget projections should assume cable's reach continues shrinking 5-10% annually. Build your streaming capabilities now so you're not scrambling when cable reach falls below viable levels for your campaigns.

Cord cutting represents a permanent structural shift in television, not a temporary fluctuation.

The surprising Q3 2025 pay TV gains require context. Several factors contributed to the one-quarter uptick:

Seasonal strength: Q3 is historically pay TV's strongest quarter, driven by NFL and college football returning. Sports remain cable's last compelling advantage over most streaming options.

Bundling strategies: Cable operators have aggressively bundled streaming services with cable packages. Charter offers nine streaming services bundled with cable, making total cancellation less attractive for some households.

vMVPD growth: Virtual pay TV services like YouTube TV drove most of the subscriber additions. These services are technically "pay TV" for measurement purposes but represent streaming behavior more than traditional cable.

Slowed attrition, not reversal: Traditional cable and satellite still lost subscribers. They just lost fewer than previous quarters. Charter losing 70,000 instead of 294,000 is improvement, not recovery.

Cord cutting will resume and accelerate for structural reasons:

Demographics: Young adults entering the market overwhelmingly prefer streaming. Older cable holdouts are aging out. The generational math guarantees continued decline.

Sports migration: Live sports, cable's last stronghold, are increasingly available on streaming. NFL on Amazon, NBA adding streaming deals, MLB on Apple TV+. As sports move online, cable's last compelling content advantage erodes.

Cost pressure: Cable operators face a negative spiral. Fewer subscribers means less revenue. Less revenue means price increases. Price increases accelerate cord cutting. The economics can't sustain current subscriber levels.

Technology adoption: Smart TV penetration has reached 85%+ of U.S. households. Streaming access requires no extra effort for most viewers. The friction advantage that once favored cable has disappeared.

By 2026, over 80.7 million U.S. households are expected to use non-pay TV services as their primary video source. By 2027, pay TV penetration is projected to fall below 30%. The Q3 2025 bump was noise in a clear long-term trend.

For advertisers, cord cutting's continuation has direct strategic implications:

Reach erosion: Cable TV's reach among adults under 50 has declined substantially. A cable-only advertising strategy increasingly misses the majority of this demographic. Businesses targeting younger consumers must include streaming in their media mix.

Audience fragmentation: As viewers spread across multiple streaming services, reaching scale requires presence on multiple platforms. Aggregated buying approaches that span many services deliver reach that single-platform strategies cannot match.

Measurement improvement: Streaming audiences are more measurable than cable viewers ever were. The shift to streaming actually improves advertisers' ability to understand campaign impact, even as it requires adapting buying strategies.

Cost accessibility: Streaming's lower entry barriers mean businesses that couldn't afford cable TV can now access television audiences. The cord-cutting trend, while challenging for cable operators, has democratized TV advertising for small businesses.

The cord-cutting statistics confirm what media buyers have observed for years: television audiences have shifted to streaming, and advertising strategies must follow.

Cable operators' bundling strategies create an interesting paradox. By including Netflix, Disney+, and other streaming services in cable packages, operators maintain subscriber relationships but undermine the value proposition of cable itself.

A household receiving streaming services through their cable bundle may watch primarily on those streaming apps rather than traditional cable channels. The subscriber counts as "cable" for measurement purposes, but viewing behavior is streaming-first. For advertisers, this means even "cable subscribers" may be better reached through streaming advertising than traditional cable buys.

The bundling approach represents cable operators managing decline rather than reversing it. They're capturing margin on streaming distribution while accepting that cable TV viewing itself continues declining among even their own subscribers.

Several indicators signal whether cord cutting is accelerating or stabilizing:

Quarterly subscriber reports: Pay attention to traditional cable and satellite losses, not just total pay TV numbers inflated by vMVPD gains. The underlying trend in actual cable subscriptions matters most for cable advertising reach.

Viewership data: Nielsen's Gauge reports show where viewing time actually goes. Even if subscriber counts stabilize, viewing time migration to streaming affects advertising reach.

Sports rights deals: As more sports move to streaming, cable loses its last compelling content advantage. Watch where NFL, NBA, and other major sports place their streaming rights.

Young adult behavior: Cord-never rates among emerging adults indicate future trajectory. If young adults continue avoiding cable subscriptions entirely, long-term decline is assured regardless of short-term fluctuations.

Industry analysts have weighed in on the cord cutting trajectory.

MoffettNathanson's report acknowledged the surprising Q3 results while maintaining bearish long-term outlook: "Yes, Q3 saw a positive net add number for the first time in eight years, but that positive result came in the year's seasonally strongest quarter. We're not yet close to seeing the category actually grow again."

The research firm posed the key question: "But might we eventually?" Their analysis suggests not, given demographic headwinds and streaming's continued expansion.

Media industry observers have noted the bundling strategy's limitations. While cable operators have slowed losses by including streaming services, this approach dilutes the value proposition of cable itself. Customers receiving Netflix, Disney+, and Max through their cable bundle are effectively already streaming users who happen to pay cable companies.

Trade publications emphasize the advertising implications. As StreamTV Insider noted, the viewing time data tells a clearer story than subscriber counts. Nielsen reported October 2025 viewing at 45.7% streaming, 22.9% broadcast, and 22.2% cable. Even among pay TV subscribers, much of their viewing happens on streaming.

Cord cutters are consumers who previously subscribed to traditional cable or satellite TV and have since canceled their subscriptions in favor of streaming services or other alternatives. Cord nevers are consumers who have never subscribed to traditional pay TV services, typically younger adults who grew up with streaming as their primary video source. Both groups represent audiences unreachable through cable TV advertising. The cord-never segment is growing as each generation of young adults enters the market without cable TV experience.

Cable operators have pursued several strategies to slow subscriber losses. Bundling streaming services with cable packages makes cancellation less attractive. Improving broadband service maintains customer relationships even when TV subscriptions end. Developing their own streaming offerings (like Peacock for Comcast) captures cord cutters within their ecosystem. Raising prices on remaining subscribers (a controversial approach that may accelerate cord cutting) maintains revenue temporarily. None of these strategies reverses cord cutting's underlying trajectory, but they help cable companies manage the transition.

The rate of decline has moderated slightly. Pay TV lost 5.8% of subscribers year-over-year in Q3 2025, compared to 6.7% the previous year. However, the industry is still losing millions of subscribers annually. Q3 2025's positive subscriber count was driven by virtual pay TV services (YouTube TV), not traditional cable recovery. Cord cutting continues; the pace has merely stabilized.

Pay TV as a category added 303,000 net subscribers in Q3 2025, the first quarterly gain since 2017. However, this gain came from vMVPDs like YouTube TV (which added 750,000 subscribers), while traditional cable operators merely reduced their losses. Comcast, Charter, and similar providers still lost subscribers, just fewer than previous quarters.

Approximately 77.2 million U.S. households have cut the cord as of 2025, compared to 68.7 million that still subscribe to traditional pay TV. Cord-cutting households now outnumber cable households. When including cord-nevers (those who never subscribed), the majority of American households don't have traditional cable subscriptions.

Cost remains the primary driver, with 86.7% of cord cutters citing high cable prices. Average cable bills of $100-150+ monthly for content bundles drive subscribers to streaming alternatives at $15-20 per service. Additional factors include better content on streaming platforms, flexibility without contracts, and superior user experiences.

Cord cutting requires advertisers to shift television budgets toward streaming platforms. A cable-only advertising strategy increasingly misses the majority of adults under 50. CTV advertising through platforms like Adwave enables reaching cord cutters and cord nevers on streaming services, often with better targeting than cable ever offered.

Traditional cable will likely survive in reduced form, serving older demographics and sports enthusiasts. However, cable's dominance has ended permanently. Projections suggest pay TV penetration falling below 30% by 2027 and continuing lower. The cable TV model that existed for 40+ years won't return, regardless of occasional quarterly fluctuations.

Key statistics on cord cutting trends and pay TV decline:

Q3 2025 pay TV subscriber change: +303,000 net (MoffettNathanson, Q3 2025)

Year-over-year pay TV decline: -5.8% (Ars Technica, Q3 2025)

YouTube TV subscribers: Approximately 9.4 million, +750,000 in Q3 2025 (StreamTV Insider, 2025)

Cable TV households 2025: 68.7 million (CableCompare, 2025)

Cable TV households 2010: 105 million (CableCompare, 2010)

Cord-cutting households 2025: 77.2 million projected (CableCompare, 2025)

Pay TV penetration 2010: 88% (nScreenMedia, 2010)

Pay TV penetration 2025: ~35% (nScreenMedia, 2025)

Cord cutters citing cost as reason: 86.7% (Evoca, 2025)

Streaming share of TV viewing: 47.3% (Nielsen Gauge, 2025)

All sources linked above. Data current as of December 2025.

Cord cutting isn't slowing down, and advertisers need strategies to reach streaming audiences. The Q3 numbers don't change the fundamental reality: television viewing has shifted to streaming, and advertising must follow.

Adwave makes streaming TV advertising accessible for businesses of any size, with campaigns starting at just $50. Reach cord cutters and cord nevers on 100+ streaming channels including Hulu, Peacock, and Discovery. Geographic targeting ensures local businesses reach relevant audiences.

No cable subscription required. No massive minimums. No production costs with AI-generated creative.

See how it works | View pricing